Sequencing Risk

When it comes to maximising retirement savings, many look to the average annual return of an investment to determine whether it has been a good or bad performer. However, the sequence (and volatility) of returns is an often overlooked factor that can have a material impact on the final balance an investor receives.

We refer to this as Sequencing Risk

What is sequencing risk?

Sequencing risk is the risk that the order (or sequence) you experience investment returns has an impact on your portfolio balance. Many investment forecasts assume a constant long run average return – however, if you are making contributions or withdrawing from your portfolio, the volatility or uncertainty around the order in which you achieve these returns does matter!

Why does it matter?

Experiencing negative returns in your investment portfolio close to significant milestones (for example, retirement age or at a time where you need to access cash) can have a significant impact on your plans, compared to having those negative returns occur earlier in your life. This is because your portfolio has less time to recover from losses, and also the losses occur when the portfolio balance is higher in dollar terms.

Experiencing these losses as you approach a critical time like retirement (what we call the Heightened Risk Zone) can mean re-evaluating your goals and the type of lifestyle you can afford to live.

Example

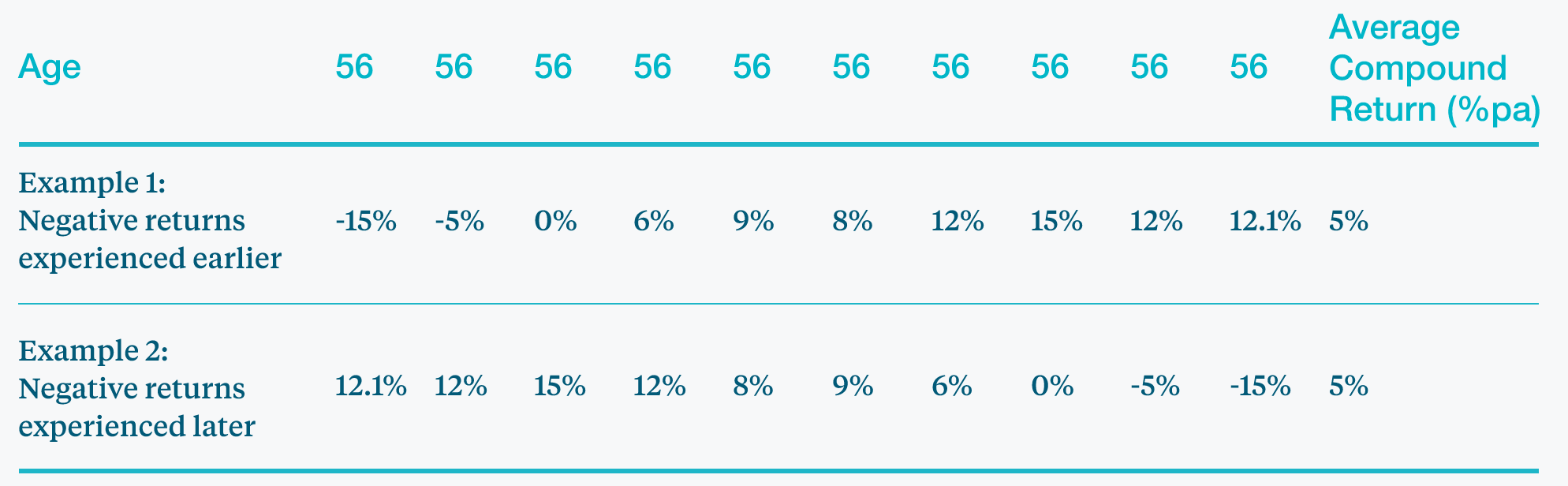

As an example, Mark is a 55 year old looking to retire in 10 years’ time. His current superannuation balance is $800,000, and he is making $25,000 in annual contributions in the lead up to his retirement.

In both of the examples below, Mark’s portfolio achieves a 5% p.a. return on average over the 10 years.

In the first example, Mark experiences negative returns early on in his investment journey, age 56 & 57, while in the second the order of returns is simply reversed, and the negative returns now occur at the end, closer to retirement.

What difference does this make to Mark’s ending balance?

Looking at the above examples you may say that in both scenarios he has an average 5% return (compounded annually) so the ending balance should be the same. However if you take a closer look and consider the impact of sequencing risk or the order in which Mark experienced the investment returns, the difference is quite impactful on the amount he has to retire on at age 65.

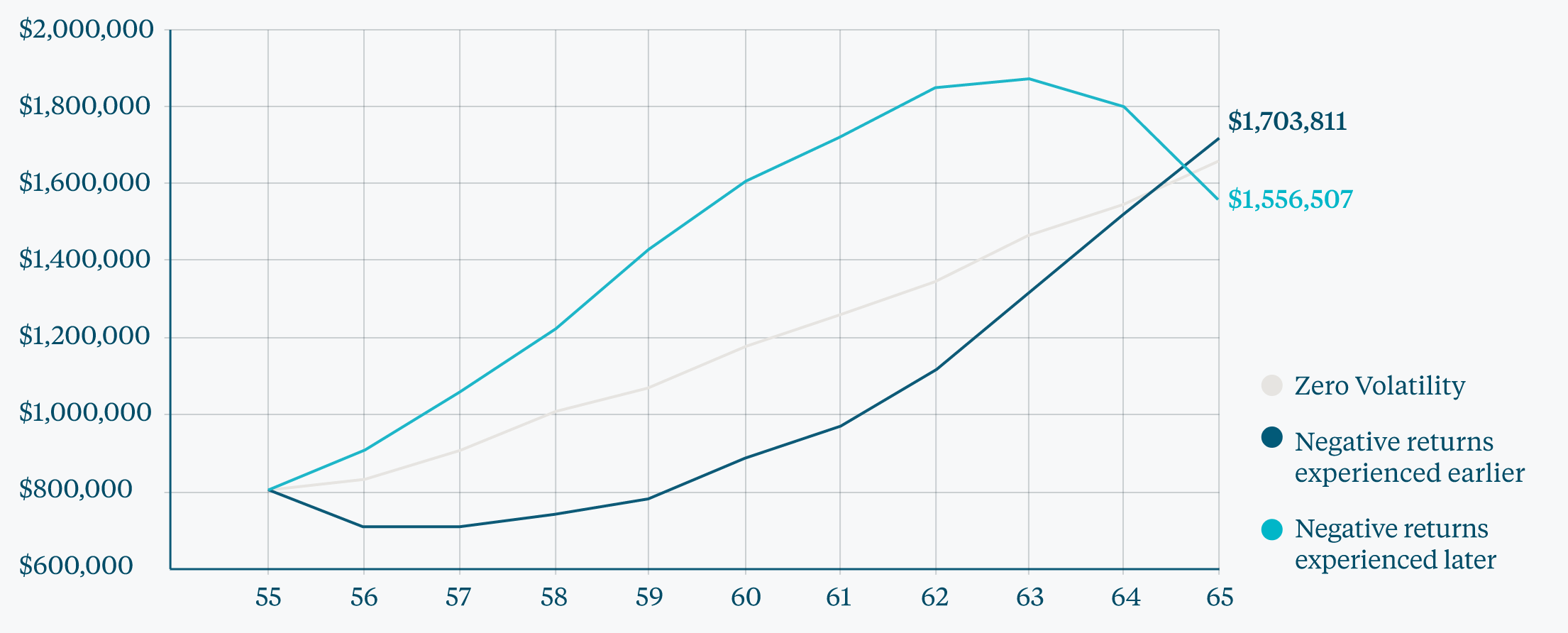

Sequencing Risk Example

Source: Atrium Investment Management

As you can see from the chart above, even though the average return is the same for both portfolios, experiencing the negative returns earlier leaves Mark with an account balance of $1,703,811, while having those negative returns later on means Mark retires with an account balance of $1,556,507 – a difference of $147,305 or 9%!

While we can’t predict the future path of returns, by having a deliberate focus on targeting the risk of a portfolio it is possible to minimise the chance of large portfolio falls (at the wrong time) and provide a smoother return profile over time.

Risk Targeting aims to managing uncertainty while also providing a higher probability of meeting your objectives.

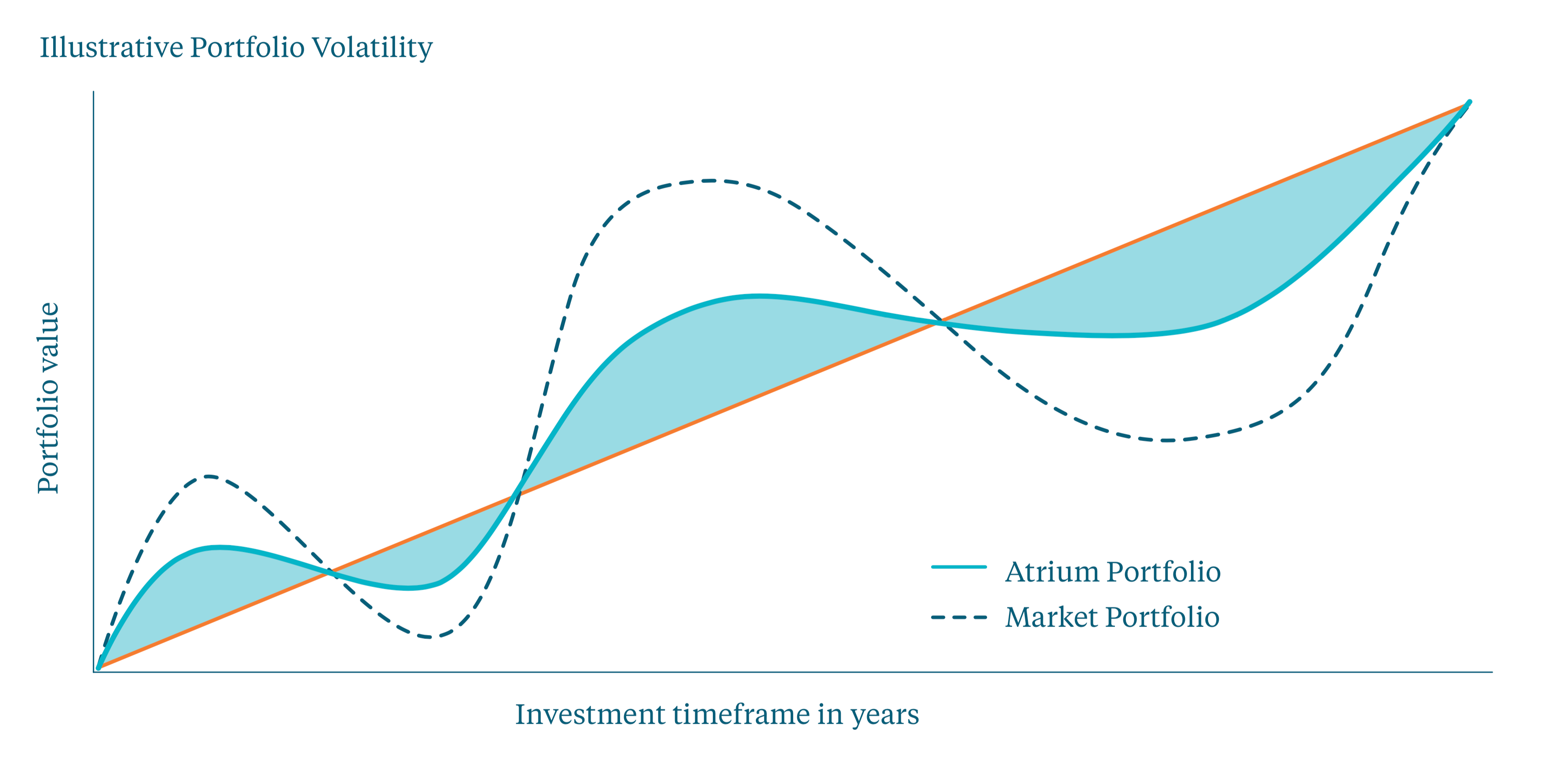

What is Risk Targeted Investing?

The Risk Targeted Approach (RTA) focuses on maximising return for a given level of risk. The approach aims to manage the Portfolio to a defined risk level (the risk target) by investing in a diverse range of assets, actively and dynamically managed.

This aims to provide a more consistent return outcome for investors.

The RTA seeks to:

-Maintain risk within agreed targeted levels over the appropriate time period

-Provide a more consistent investment return outcome

-Preserve client capital (minimise capital loss)

Source: Atrium Investment Management

By seeking to preserve capital during market downturns, clients can then benefit more from compounding returns in positive market environments.

The overall aim of Atrium’s approach is to seek the safest way to achieve clients’ objectives over their investment timeframe.

While we all want the highest return possible when we are making an investment, Risk does matter and should always be a major consideration when developing a portfolio which will stand the test of time.

Important Information

The information in this document (Information) has been prepared and issued by Atrium Investment Management Pty Limited (ABN 17 137 088 745, AFSL 338 634) (Atrium). The Information is provided for the use of licensed and accredited financial advisers only. In no circumstances is it to be used by a potential client for the purposes of making a decision about a financial product or class of products. The Information is of a general nature only and does not take into account the objectives, financial situation or needs of any person. No liability is accepted for any loss or damage as a result of any reliance on the Information. Past performance is not a reliable indicator of future performance. Future performance and return of capital is not guaranteed. While every care has been taken in the preparation of the Information, Atrium makes no representation or warranty as tothe accuracy or completeness of any statement in it including without limitation, any forecasts. This document contains projections, forecasts, targeted returns, illustrative returns, estimates, objectives, beliefs, back-testing, hypothetical returns, simulated results, non-actual and similar information (Non Actual Information). Non Actual Information is predictive in character, may be affected by inaccurate assumptions or by known or unknown risks and uncertainties, and may differ materially from results ultimately achieved. Non Actual Information involves subjective judgment and analysis, the use of historical long term data and most recently available data obtainable from independent sources, and is subject to assumptions that Atrium management believe to be reasonable, but that can be inherently uncertain and unpredictable. Non Actual Information is provided for illustrative purposes only and is not intended to serve as, and must not be relied upon as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Some important factors that could cause actual results to differ materially from those in any Non Actual Information include changes in domestic and foreign business, market, financial, political and legal conditions, and incorrect data provision by external sources. There can be no assurance that any particular Non Actual Information will be realised.