CIO Note: Setting the Compass

Managing Money Through Wars, Headlines and Geopolitics

The headlines at the moment are difficult to read. Conflict in the Middle East. The Strait of Hormuz back in the news. Tariffs, trade and domestic politics. And yet the S&P 500 and NASDAQ are at or close to all-time highs. For investors, that disconnect can be uncomfortable, and it is the right time to pause and take stock.

What we are aiming to achieve, in times of uncertainty, and always

Everything we do flows from a clear set of objectives, and it is worth restating them.

Our multi asset portfolios aim to achieve both a return objective and a risk objective that results in a portfolio that behaves consistently through changing market conditions, designed to draw down less during market dislocations, and recover when conditions normalise to facilitate the long-term compounding of returns.

This investment approach aims to buffer market volatility and deliver a smoother return profile through market cycles, and to provide investors with the confidence to stay invested through periods of market dislocation such as we are currently experiencing.

A smoother path of returns does not mean portfolios will avoid every bout of short-term volatility — particularly when we have good reason to expect strong medium‑term returns. Nor are we trying to dodge every market wobble. At times, short‑term volatility is simply the price of being invested, and that is something we can accept. What we are determined to avoid is permanent loss of capital and the long, painful recovery periods that can follow when markets sell off hard and stay down.

The way we manage this is two-handed. We anchor portfolios to our medium- to longer-term views, and we manage risk in the near term — through diversifiers, hedges and dynamic positioning — so that a tough few months in markets does not undermine the long-term plan.

That way we aim to deliver on our objectives and provide greater confidence in the outcomes of our investment approach, regardless of what is going on in the global economy and markets.

The world we are investing in

Wars are humanitarian disasters. They are usually not market disasters

More than a century of conflicts shows a pattern that indicates that outside of world wars, the market impact is typically regional, sector-specific, and shorter-lived than the headlines can suggest. A few examples make this point:

- Korean War (1950–53): the Dow fell ~13% in the three weeks following the invasion and recovered within two months. The S&P Composite index of the day rose around 50% over the course of the ~37-month war.

- Cuban Missile Crisis (1962): markets fell ~7% over 13 days, then recovered fully within three months.

- Gulf War (1990–91): the S&P 500 sold off ~17% as Iraq invaded Kuwait, then rallied roughly its way back through Q1 1991, with the S&P 500 trough-to-late-March move of around 25%, and pre-invasion levels regained by mid-February.

- 9/11 (2001): markets fell ~12% on re-opening and were back to pre-attack levels within a month.

- Russia–Ukraine (since 2022): an early shock and the most recent example of markets pricing risk to regions and sector; on outbreak the S&P 500 has a single day drop of ~1.8% but finished the week +0.8%; the dominant driver of equity returns since has been inflation, AI and earnings, not the war itself.

To date we are seeing the same pattern now. Despite Israel–Iran, the Strait of Hormuz, and a backdrop that genuinely feels uncomfortable, the S&P 500 and NASDAQ are at all-time highs after initially falling. US large-cap concentration has been a positive in this instance— much like the technology led Mag 7 were through the post-Covid era. When the world looks fragile, capital can gravitate to the deepest, highest-quality earnings streams it can find.

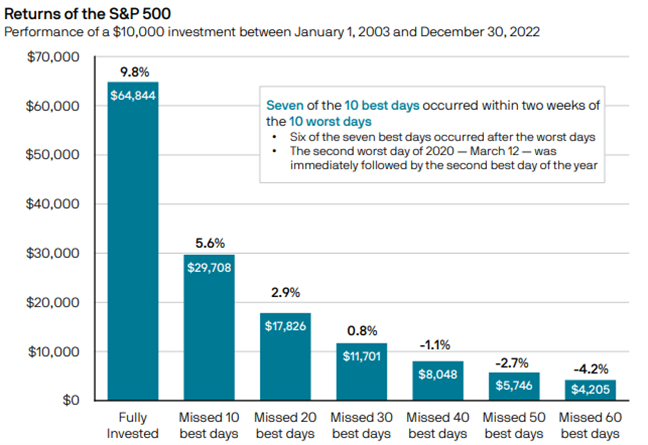

Time in the market beats timing the market – by a long way

This is an important lesson, and it is the reason we do not try to time markets but manage risk to smooth the path. The cost of getting it wrong is large.

JP Morgan Asset Management research highlights a key point of investing. Over the 20 years to the end of 2022, a fully invested $10,000 in the S&P 500 grew to roughly $65,000.

- Missing just the best 10 days reduced that to ~$30,000.

- Missing the best 30 days would leave ~$11,700 — barely above the starting capital.

- Missing the best 50 days would have reduced the investment to under $6,000.

The reason this matters is the best 10 days almost always sit within two weeks of the worst 10 days. The moments when investors are most tempted to sell are precisely the moments around which the best returns are made.

Our approach seeks to avoid this painful outcome — we can accept short-term volatility as the price of being invested, and we use risk-management tools (hedges, diversifiers, dynamic tilts) to limit drawdown without stepping out of markets at the wrong moment.

Why are markets where they are given all the uncertainty?

From our perspective, two reasons stand out. First, investors are pricing a resolution in the not-too-distant future. President Trump wants a resolution, and ultimately so does Iran. Both countries are negotiating. Crude oil forward curves are in significant backwardation — that is, the market is paying more for oil today than for oil in twelve months — indicating the market believes the energy disruption is temporary, not a structural shift.

Second, the underlying economy and earnings remain strong, particularly in the US. This provides a buffer to global growth and energy led inflation, provided the conflict does not become prolonged. Corporate earnings revisions and guidance were positive into the conflict and have been strong since. That earnings support is a key pillar of our constructive outlook, even as geopolitical risks continue to dominate headlines.

The US economy is in good health, supporting global markets, which is driving our positioning

We continue to expect we are in a mid-cycle expansion in the US: employment is balanced, corporate profits are strong, financial conditions are supportive, and fiscal policy is a tailwind. Underneath that cyclical picture is a set of structural drivers we think are highly impactful:

- AI and the productivity story — adoption is broadening from the largest tech names into the broader economy, and this has the potential to lift margins and capital investment

- Reshoring, defence and national-security spending — a multi-year fiscal tailwind into domestic manufacturing, grids and supply chains

- Deregulation — quieter, but a real tailwind to the financial sector and corporate activity

- A services-led economy that is far less cyclical than the goods-and-housing-led economy of the past

- Energy self-sufficiency — an important risk consideration is that the US is energy self-sufficient; while prices may be higher, the risk of an energy shortfall is avoided and economic activity can continue

This is different to other parts of the world such as Europe and Australia, where cyclical exposure is higher, the energy import position is weaker, and the productivity / fiscal story is thinner. It is part of why we continue to favour the US within global equities.

Summary

The positioning of our multi-asset portfolios reflects the same logic and is why our portfolio volatility may currently be higher versus similar sized bouts of market volatility historically. We see a real risk of trying to time markets in the event of a resolution to the Middle East conflict given we expect a resolution will be forthcoming and the US economy is performing very strongly. There is a better way to protect the portfolios without sacrificing the opportunity to participate when conditions improve.

Indeed, it is in moments like this — when the headlines are loud and markets seem to defy them — that the value of experience and a fundamental framework, coupled with a disciplined, multi-asset, risk-targeted approach counts.

We are not trying to predict whether the war ends in three weeks or three months, or whether the Fed cuts in June or August.

We are positioning for the most probable path, managing near term risks, hedging the tail, and staying invested so portfolios deliver the results we expect them to over time.

Tony Edwards

Chief Investment Officer

Important Information

The information in this document (Information) has been prepared and issued by Atrium Investment Management Pty Ltd (ABN 17 137 088 745, AFSL338634) (Atrium). The Information is intended for use by financial advisers and wholesale investors only. Retail investors should not rely on any information in this document without first seeking advice from their financial adviser. This document has been prepared without taking into account your individual objectives, financial situation or needs. Past performance is not a reliable indicator of future performance. The return of capital is not guaranteed.

Performance figures relate to the portfolios managed by Atrium. Individual investor portfolio performance may be different from the results above and will differ among clients depending on the timing of their investment and the level of variation from the models. Performance is net of investment management fees, does not take into account platform administration fees that may apply, and may not take into account some or all of the rebates you may receive.